Basic Budgeting for Beginners: Implement the 50/30/20 rule, control your spending, reduce your debt, and increase your emergency fund.

What a Budget Is and Why It Works Right Now

A plain definition that works in real life

A budget is a monthly plan that tells every dollar where to go before you spend it, so today’s choices line up with what you want most next month and next year.

Think of it as a map you drew for yourself, because when intention is clear, execution feels lighter and more sustainable.

Three immediate wins for beginners

You finally see where money flows, you prevent repeat surprises, and you create space for savings even with a modest paycheck.

Clarity lowers guilt around planned spending, predictability eases bill stress, and a growing cushion boosts emotional security.

Why simplicity beats complexity at the start

Complex systems demand time and energy you may not have, while a simple method keeps working during busy or chaotic weeks and guarantees steady progress.

Core Principles of a Simple Budget

Clarity before micrometer precision

Clear categories beat perfect but confusing ones, so prefer broad groups and easy names from day one.

Fewer categories with a learning purpose

Group spending into Needs, Wants, and Savings & Debt, then add subcategories only when they meaningfully guide decisions.

A short weekly review that keeps you on the rails

Set a fixed 10-minute slot once a week to update entries, scan your bank feed, and tweak the plan, because frequent tiny corrections prevent end-of-month storms.

Treat surprises as a recurring cost

Feed a small “unexpected” line every month, since real life produces surprises often enough that they deserve a standing place in your plan.

Give every dollar a job in a stable order

Protect the essentials, limit the optional, and fund goals on schedule, because the sequence of decisions drastically changes results.

The 50/30/20 Method in Plain English

The three buckets that remove daily friction

Fifty percent to Needs, thirty percent to Wants, and twenty percent to Savings & Debt is a simple ratio that removes guesswork and reduces everyday decision fatigue.

Needs — the costs that keep life functioning

Housing, basic groceries, transportation, utilities, insurance, and anything truly required for work or school belong here because the day collapses without them.

Wants — quality of life within healthy limits

Dining out, entertainment, nonessential clothing, hobbies, and small treats live here so the plan remains human and sustainable rather than punishing.

Savings & Debt — the future funded every month

Emergency fund contributions, extra debt payments, and specific goals should be automated when possible, turning intentions into predictable action.

Adjusting ratios without losing the logic

If your town is expensive or income is tight, shift the percentages temporarily while keeping the core logic intact: protect Needs, cap Wants, and pay yourself first.

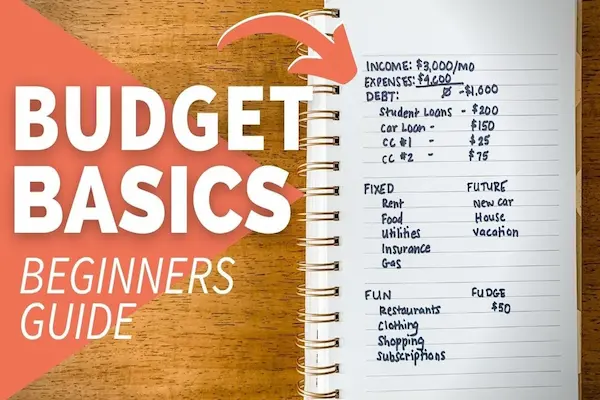

A Full Example with $3,000 Net Monthly Income

One coherent allocation you can test for two or three months

At $3,000 take-home pay, 50/30/20 suggests $1,500 for Needs, $900 for Wants, and $600 for Savings & Debt.

A practical Needs setup could be Rent $900, Basic Groceries $350, Transportation $150, and Utilities $100, which closes the bucket cleanly.

Wants could be Restaurants $250, Entertainment $150, Clothing $100, Hobbies $100, Personal Care $100, and Flex $200 to absorb weekly swings.

Savings & Debt could allocate Emergency Fund $300, Extra Debt Paydown $200, and Specific Goals $100, which moves you forward without strangling the present.

Scaling the same logic to different paychecks

At $2,000 net, the buckets become Needs $1,000, Wants $600, and Savings & Debt $400, preserving the same decisions with smaller numbers.

At $4,000 net, Needs $2,000, Wants $1,200, and Savings & Debt $800 let you accelerate savings and widen your margin.

The quiet power of a built-in buffer

The Flex line inside Wants is a shock absorber that catches invitations and tiny price bumps so the overall plan does not crack.

Your Copy-Ready Budget Worksheet

The essential fields to keep you organized

Write your Monthly Net Income, your 50/30/20 Targets, your Needs list, your Wants list, and your Savings & Debt plan, plus a Weekly Check-In box and a Monthly Notes box.

Record target values, actual values, and the difference, then note one adjustment for next week so lessons turn into action.

How to fill it without getting stuck

Start with income, compute the three buckets, list fixed costs, and estimate variable lines using the last month as a reference, remembering to add an “unexpected” mini-fund.

Round to the nearest five or ten dollars at the start to reduce friction, because precision improves naturally as you review each week.

A tiny routine that protects momentum

In ten minutes, update two or three new charges, compare totals to your targets, and decide one small change for the next seven days to keep the plan alive.

How to Track Expenses Without Headaches

Low-effort digital methods for practical people

A quick manual-entry phone app builds awareness the moment you spend, while a minimalist spreadsheet summarizes the month with zero fancy formulas.

Phone reminders at night help you record variable purchases even on hectic days, which preserves accuracy with minimal effort.

Analog options for pen-and-paper learners

A small notebook with one page per month works for people who think better while writing, as long as the weekly time slot is sacred.

A visible whiteboard with three columns—Needs, Wants, and Savings & Debt—keeps the plan in sight so you remember to follow it.

Envelopes for taming slippery categories

Envelope budgeting assigns a limit to restaurants or entertainment, and you only spend what the envelope contains, which reduces impulse overshoots.

Digital envelopes mimic the same idea inside an app or sheet and allow controlled transfers inside the same bucket when priorities shift.

When routine fails for a day, restart without shame

If you miss a day, restart the next one, because imperfect consistency beats the perfectionism that leads to quitting.

Emergency Fund and Goal-Based Saving

A staged path that actually fits a beginner’s life

Aim for an initial $1,000 as a fast psychological and practical cushion, then build toward three months of Needs with automated monthly contributions.

If six months of Needs is your long-term target, approach it calmly and steadily rather than promising unrealistic jumps that create burnout.

Automation removes the “I’ll do it later” trap

Schedule transfers at the start of the month as if they were bills, because end-of-month leftovers rarely exist in the real world.

Give each goal a name and deadline, since “$600 for a certification in three months” motivates more than “save when possible.”

Clarity for short, medium, and long horizons

Short-term goals need near-term milestones, medium-term goals demand contribution discipline, and long-term goals belong after the emergency fund has real traction.

Paying Down Debt Without Losing Momentum

Avalanche method for mathematical efficiency

Pay minimums on all accounts and direct extra cash to the highest interest rate first, which lowers total interest and shortens payoff time.

When that balance is gone, roll its payment into the next target to create a positive domino effect.

Snowball method for psychological traction

Attack the smallest balance first to earn quick wins, free energy, and build a habit that can survive six months or more.

Visible progress strengthens discipline, and discipline over time typically beats theoretical differences between methods.

Choosing the method you can actually sustain

Pick the approach you can keep for half a year, because the best strategy is the one you can live with calmly and consistently.

Practical negotiation and organization tips

Ask about interest reductions and extended timelines when you are current on minimums, review contracts, cut useless fees, and write due dates on your worksheet so nothing slips.

Variable, Seasonal, and Sinking Funds

Why predictable non-monthly costs deserve monthly savings

Textbooks, gifts, travel, maintenance, and taxes may not show up every month, but they are predictable enough to earn their own “sinking funds.”

Small monthly deposits prevent one event from wrecking your entire plan.

A simple setup that makes timing painless

Pick three to five relevant sinking funds, assign realistic monthly amounts, and feed them automatically at the start of the month.

When the expense arrives, pay with the dedicated fund and record the movement so the current month stays intact.

Subscriptions, Fees, and Invisible Leaks

A quarterly inventory that plugs silent losses

List subscriptions, packages, and insurances with price, renewal date, and actual usage, because tiny recurring debits add up surprisingly fast.

Cancel what you do not use, renegotiate what is overpriced, and bundle services when sensible to free space inside Wants and reinforce Savings.

Alerts and reminders that shield your plan

Create a quarterly reminder to review subscriptions, enable unusual-purchase notifications, and scan for duplicate charges to reduce loss without extra workload.

Common Mistakes and How to Avoid Them

Over-categorizing and burning out on control

Too many categories feel like mastery but create friction and fatigue, and fatigue leads to abandonment, so keep the design lean.

Ignoring joy and making the plan unsustainable

Without room for pleasure, the budget becomes punishment, and punitive plans rarely survive hard months, so keep Wants honest and bounded.

Saving only if money is left over

End-of-month saving almost never happens, which is why automated first-of-month transfers are your best friend.

An invisible plan that you forget to follow

Keep the worksheet visible, use weekly reminders, and run a 10-minute check-in, because seeing the plan lowers the mental effort of remembering what to do.

Adapting When Needs Exceed 50 Percent

Three fronts to regain balance without extremes

Renegotiate contracts and plans, replace costly habits with cheaper same-purpose alternatives, and track small wins that add up over a year.

A $15 or $25 monthly reduction looks tiny in isolation but compounds into real space for savings and calm.

Protecting the health of the plan during adjustments

Trim Wants temporarily without eliminating all fun, preserve a minimum of breathing room, and restore ratios as relief appears to avoid a yo-yo effect.

Simple metrics that keep motivation honest

Write down the Needs percentage each month, log completed renegotiations, and note which habits you successfully swapped so progress stays visible.

A 30-Day Starter Plan with Weekly Milestones

Week 1 — Map and choose your rails

List true net income, compute your three buckets, write fixed costs, and estimate variables using the last 30 days as a guide.

Set three one-line goals such as “no late fees,” “save $200,” and “cap restaurants at $250,” keeping focus on what matters.

Week 2 — Make it visible and automate the hard parts

Build your worksheet, choose one main tracking method and one backup, and place your plan where you will see it daily.

Schedule saving transfers and any eligible auto-pays so memory is not responsible for success.

Week 3 — Fine-tune and launch sinking funds

Check remaining balances per bucket, reallocate inside the bucket, and start two sinking funds with small, steady contributions.

Test envelopes for your slipperiest categories to keep spending within rails without micromanaging every purchase.

Week 4 — Consolidate and set your long-term rhythm

Run a subscription inventory, negotiate one overpriced bill, and close the month with a one-page “lessons and next month priorities” note.

Set a monthly close-out reminder and a quarterly deep review so cadence supports the habit for many months.

Quick Answers to Common Beginner Questions

Should I start with 50/30/20 or envelopes

If you need a simple high-level map, start with 50/30/20, and if your problem is runaway variable spending, add envelopes to tighten those lines.

How long until my emergency fund feels comfortable

Build the first $1,000, grow to three months of Needs, and move toward six when income allows, celebrating milestones to protect motivation.

Should I pay debt first or save first

Stay current on all minimums, build a small operating cushion, and send the extra to your highest interest or smallest balance depending on the method you can stick to.

What if my income varies month to month

Use a three-month average to plan, rank priorities in order, and adjust weekly, trimming Wants first when you hit a lean patch.

What if a whole month goes off the rails

Restart next month with written lessons and two or three concrete adjustments, because the skill of budgeting grows from practice rather than single-month perfection.

Ten-Minute Weekly Checklist

-

Update your worksheet with new transactions and close category totals.

-

Reconcile against your bank feed and scan for duplicates or unusual charges.

-

Compare actual spending to the 50/30/20 targets and tweak next week’s plan.

-

Confirm that saving transfers and bill payments are scheduled and funded.

-

Review subscriptions and fees if anything looks off since last week.

-

Top up sinking funds that are running low.

-

Write one practical lesson and one specific commitment for the next seven days.

A Complete $3,000 Monthly Model You Can Copy

Needs — $1,500 total

Rent $900, Basic Groceries $350, Transportation $150, Utilities $100, and a small school or work essentials line that can vary between $0 and $100.

Keep the bucket within $1,500 by compensating differences with trades inside the same bucket.

Wants — $900 total

Restaurants $250, Entertainment $150, Clothing $100, Hobbies $100, Personal Care $100, and Flex $200 to absorb natural swings.

If one subcategory runs hot, pull from Flex or trim another Want rather than touching other buckets.

Savings & Debt — $600 total

Emergency Fund $300, Extra Debt Paydown $200, and Specific Goals $100, with first-of-month transfers to guarantee execution.

When a goal completes or a balance is cleared, roll the freed amount into the next priority to maintain momentum.

Mini Glossary for First-Timers

Net income is the money that actually lands in your account after taxes and mandatory deductions.

Fixed expenses repeat with predictable amounts such as rent, utilities, and subscriptions.

Variable expenses change with usage and choices such as restaurants, entertainment, and small purchases.

An emergency fund is a savings cushion for true surprises, typically three to six months of Needs.

A sinking fund is targeted savings for a predictable non-monthly cost like maintenance, travel, or textbooks.

Avalanche is a debt method that attacks the highest interest rate first to minimize total interest.

Snowball is a debt method that attacks the smallest balance first to create quick wins and sustain motivation.

Envelopes are practical spending limits per category using cash, digital buckets, or a simple spreadsheet.

Practical Resources Without Links

Use a small notebook as your analog worksheet with one page per month and one line per transaction to keep maintenance simple.

Build a three-tab spreadsheet—Plan, Actuals, and Close-Out—with totals per bucket and “difference” fields for fast course correction.

Set two phone reminders, a weekly 10-minute review and a monthly close-out, because reminders turn good intentions into habits.

Create separate envelopes for restaurants and entertainment, fill them at the start of the month, and honor the limit like a promise to your future self.

Print a one-page checklist and place it near your desk so the plan stays inside your daily field of view.

Executable Summary in a Few Lines

Calculate your 50/30/20 buckets from net income and fill a simple worksheet with Needs, Wants, and Savings & Debt.

Automate transfers to emergency fund, debt paydown, and named goals at the start of the month.

Track variable spending with a low-friction method and run a weekly 10-minute check-in to correct early and often.

Treat surprises as a recurring cost with sinking funds, review subscriptions quarterly, and adjust without guilt because consistency beats intensity.

Closing Motivation for Beginners

A simple budget is a flexible map that protects what matters, keeps joy in the plan, and funds your goals with steady progress even on a modest income.

With 50/30/20, a visible worksheet, and a short weekly routine, you create a system that fits your real week and keeps working when life gets loud, precisely because it is designed to be light and repeatable.

Start with this month, welcome imperfect learning, and keep adjusting the route, since financial stability comes from many small good choices repeated calmly over time.